Can Muslims get a mortgage?

Is a mortgage allowed in Islam?

Islamic scholars generally agree that it is not permissible for Muslims to buy a home using a traditional mortgage loan. That is because at the heart of a traditional mortgage is riba, the practice of lending and borrowing money at interest.

Some scholars say a traditional mortgage may be permitted under extenuating circumstances, where buying a home is considered a need and no alternative to a mortgage exists. However, Islamic finance alternatives to a mortgage now exist in the West. Where reasonable alternatives exist, the exception would not apply.

For faith-conscious Muslims, Islamic home financing is clearly the way to go when buying a house.

Muslims can get an alternative mortgage if it’s shariah-compliant.

Shariah-compliant alternatives to a mortgage do exist, and they are now not only accessible in America but competitively priced as well.

What is an Islamic mortgage?

An Islamic mortgage are based on an entirely different foundation from a traditional mortgage loan. A halal mortgage is not a loan at all, but an entirely different type of business transaction based on principles that are acceptable under Islamic law.

How can you ensure that your home financing is sharia compliant?

With a little research, you can ensure that your home financing truly complies with sharia law.

- First, choose a home financier that solely provides Islamic home financing. It’s best to avoid choosing a bank that provides so-called Islamic mortgages on the side while engaging in many activities that are not halal. Read more about why below.

- Then, check that the financier’s services are riba-free. The entire foundation of the financing should be structured on sound Islamic approaches. The preferred option in the West is a co-ownership arrangement, known as musharakah, in which the customer and financier buy the house together as partners.

- And finally, ensure that the financier is approved by a reputable board of Islamic scholars.

Be aware that some of the terminology used in the material on Islamic home financing may resemble that used in traditional mortgages, such as the term “rates.” That does not mean that it’s not halal. Islamic home financing must comply with government regulations, and it may be structured in a way that makes it easy for customers to compare with traditional options. What you are checking is the underlying structure and foundation.

As a quick analogy: Two bags of potato chips might look similar, but once you look at the ingredients, you may find that one is made with lard and is not halal, while the other is made with vegetable oil and is halal for you to enjoy.

Check the ingredients of your home financing. They should be clearly explained on the company’s website.

>> Related Read – What Is An Islamic Mortgage? How Does It Work?

Conventional home loans are not permissible in Islam.

It’s important to understand that the entire system underlying conventional home loans is haram, as well as the loan itself.

A loan in Islam is intended to be a charitable arrangement — a way to help another person without seeking gain or profit. Profiting from a loan through riba, or interest, is prohibited. The entire foundation of a conventional mortgage loan rests on the use of interest, so alternative Islamic financing solutions are clearly necessary.

There are additional reasons beyond riba, however, that make a conventional mortgage impermissible under Islamic law.

Asset backed finance

Under Islamic financing principles, another of the most important principles in Islamic finance is that it is asset-backed finance. A person can only buy or sell an asset that has intrinsic value. Money has no intrinsic value; it is only a medium of exchange. In a conventional loan, the customer is actually buying the use of money in return for more money later. It’s like agreeing to buy $20 for $30. This is not an acceptable financial contract in Islam.

This prohibition protects the market’s stability and protects against manipulation.

Equity and justice

Islamic financing protects individuals from exploitation and harm and fosters equity and justice. A borrower-lender relationship is inherently unequal in power. This places customers at risk of exploitation since they have no choice but to agree to the lender’s terms, with only government regulations—which vary from state to state and can change at any time—to protect them.

Halal sources of income

Finally, money in Islam must be gained in a halal manner. Banks that provide their own version of Islamic mortgages in additional to conventional mortgages have earned the money they provide their customers through the use of interest, as well as through investing in and engaging in a range of other activities that are not permitted in Islam. This renders the use of that money problematic for Muslim consumers.

With so many ways that a traditional mortgage runs counter to Islamic financial practices, it’s good that sharia compliant mortgages now exist for faith-conscious Muslims in America.

>> Related Read – The Difference Between an Islamic Mortgage and a Conventional Mortgage

Watch out: Not all Islamic home financing options are shariah compliant.

When you make the intention to choose Islamic home financing, you have made an important first step. Now, you will want to follow up and ensure that the service or product you’re choosing is actually shariah-compliant. The authenticity of the product is essential.

Here are some important questions to keep in mind as you consider different Islamic financiers:

- Is the financier an Islamic organization that understands the nuances of Islamic law and shariah-based financial principles?

- Was the company’s home financing product developed under the oversight of Islamic scholars?

- Is the company audited on a regular basis by experts in Islamic finance to ensure that their practices remain halal?

This information should be clearly stated and supported on the company’s website. A few minutes of research are all it should take to check the company’s history and the authenticity of its product.

Explore Muslim home financing options.

Fortunately, choosing a halal mortgage does not mean a customer is limited in terms of choices and options. On the contrary, an array of halal mortgage options are now available.

A customer can choose their contract length, the percent of the home’s price they will pay as a down payment, and even whether their rate is fixed or adjustable. They can finance any type of home, from a condo to a single-family home, and even a second or vacation home.

Choose the #1 U.S. Islamic home finance provider.

For many years, many Muslims in America rented homes for their entire lives, finding no way to achieve the stability that purchasing a home can offer. That’s why Guidance Residential was founded, offering halal mortgages for these families who previously saw no way to buy a home.

More than 20 years ago, Guidance Residential pioneered an authentic model of Islamic home financing that opened the world of homeownership to American Muslims as well as others who appreciate the benefits of this more just and equitable alternative to a traditional mortgage.

Since then, the company has enabled more than 40,000 families to enjoy the benefits of homeownership.

How does it work?

Guidance Residential’s authentic model of faith based financing creates an LLC for every home purchased. Guidance and the home buyer purchase the home together as co-owners, each owning a percentage in accordance with the amount of money each side contributes.

Over the course of a contract length chosen by the customer, the home buyer gradually buys Guidance’s shares of the home. Home buyers make monthly payments consisting of two parts — one portion allowing the customer to acquire an increasing share of the home, and the other part compensating Guidance in return for using their portion of the property.

What are the benefits?

Most importantly, Guidance Residential’s customers enjoy the peace of mind that comes with knowing that they have chosen a true riba-free and sharia compliant Islamic mortgage.

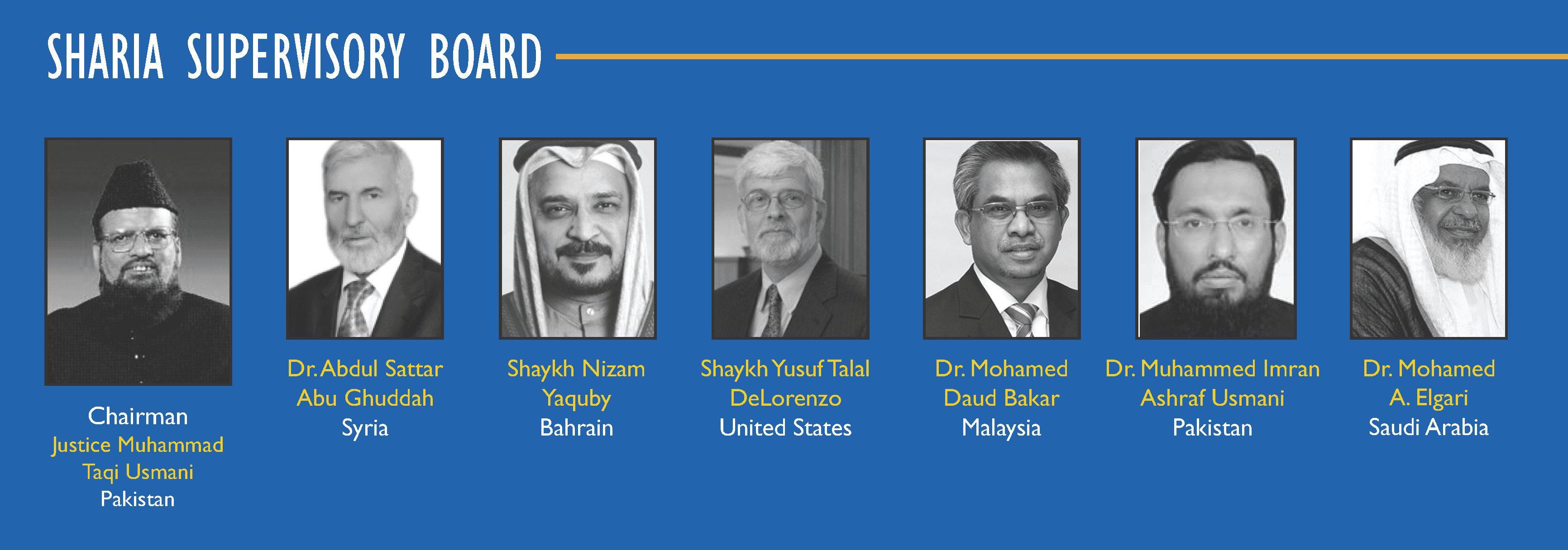

Guidance was not only founded with the help of a panel of Islamic scholars, but it is overseen and audited each year by an independent shariah board to ensure that its services continue to adhere carefully to sharia law.

But beyond that, Guidance Residential’s customers enjoy additional benefits as well.

Additional benefits

First, the homeowner enjoys full ownership rights from the beginning, with their name on the title to the home.

Second, Guidance Residential shares some of the risks of homeownership in a way that a mortgage lender does not, in case of natural disasters, eminent domain or foreclosure.

Third, Guidance Residential does not charge any pre-payment penalty for paying off the home early; nor does it profit from fees beyond a small administrative fee for late payments.

>> Explore Guidance Residential’s available options now.

We wish you the best on your home-buying journey!

Your Guidance Residential Account Executive is here to help with any questions. Looking to refinance or purchase? Have a friend or family member who is looking for a home? Call 1.866.Guidance, or start an application online today!

Blog originally posted on November 18th, 2020. Updated on September 11, 2023.