Is It Better to Put a Large Down Payment on a House?

When you’re in the market for a new home, most people will advise you to put as much money down as possible.

It’s common to hear advice to do whatever you can to save up for the down payment, even to the point of assuming that a 20 percent down payment is standard for home loans.

Believe it or not, a large down payment isn’t always necessary—or even wise. Let’s take a look at the truth behind the many rumors regarding this important part of the home financing process.

What Is a Down Payment?

A down payment refers to the upfront payment the buyer makes when buying a home, typically in the form of cash. In the context of a home purchase, a down payment is a percentage of the total purchase price that the buyer pays upfront, reducing the amount that they will need to finance with the help of a home finance company.

The size of the down payment can significantly affect the terms of the mortgage. A lower down payment will often result in a higher monthly payment for the homeowner.

Advantages of a Large Down Payment

Is it better to have a bigger down payment? It can be. A major reason is that the size of a down payment significantly impacts the monthly mortgage payments on a home. Generally, the larger the down payment, the lower the monthly mortgage payment will be.

The mortgage loan amount is determined by subtracting the down payment from the purchase price of the home. For example, if a home costs $200,000 and the buyer makes a down payment of $40,000 (20% of the home price), the mortgage loan would be $160,000. If the down payment were only $20,000 (10% of the home price), the mortgage loan would be $180,000. So a larger down payment reduces the loan amount and consequently results in more manageable monthly payments.

Here are some more key reasons why a higher down payment can be beneficial:

- A large down payment can mean lower (or no) private mortgage insurance. Home financing companies will typically require buyers to purchase private mortgage insurance (PMI) for home loans that have less than 20 percent down. This insurance protects the lender, not the buyer. A low down payment can lead to money needlessly spent on insurance that doesn’t technically benefit you. A higher down payment can pay off by allowing you to avoid mortgage insurance increasing your monthly payment.

- A lower LTV. LTV, or Loan-To-Value ratio, is calculated by dividing the mortgage amount by the appraised value of the property.A lower loan-to-value ratio means that you will owe less on your home. This makes you become attractive to lenders and also means you’ll get more equity faster.

- Better chances at approval. A sizable down payment generally can get you approved in situations where it would be difficult to get that “yes!” from a home financing company.

- Lower interest rates. A lower LTV ratio makes you more attractive and less risky to mortgage lenders. This is because a borrower who has invested a significant amount in the property upfront is less likely to default on the loan. This means you get to reap the rewards in the form of a lower mortgage interest rate (or profit rate, in the case of Islamic home financing). Lenders often offer better rates to borrowers who make larger down payments. This further reduces the homeowner’s monthly mortgage payment.

- Less interest paid overall. A higher portion of the loan paid off, plus lower interest rates mean you can save tens of thousands of dollars in interest on the course of your home loan.

- Lower monthly payments. This is the most commonly-cited perk of larger down payments. Less interest and less principal means that your monthly mortgage payments will be noticeably smaller.

- It may be required. A traditional loan generally requires a minimum of 20 percent down. If you want to get a co-op purchase financed or a second home in certain parts of the country, you may need a down payment as high as 30 percent or more.

Overall, while a larger down payment requires more cash upfront, it can lead to significant savings in the long run through lower monthly mortgage payments and potentially lower interest rates.

Does a Higher Down Payment Make Your Offer Stronger on a House?

The answer is “yes”. A higher down payment can make a huge impact on your offer. If you live in a hot housing market (or are trying to live in one), one of the best things you can do is offer a higher down payment for the home purchase. Believe it or not, sellers generally prefer buyers who have higher down payments—or better yet, cash to buy the home.

The reason why is simple. When you are buying a home using a mortgage loan, there is always the chance that lenders may change their minds at the last minute. This means low down payment offers tend to be unnecessarily risky. No one wants to have to start the sales process over again. In a competitive housing market, the seller can simply choose another offer.

As a result, a high down payment is a sign of a more secure transaction. That will always remain more attractive to people who want their home off the market fast.

Disadvantages of a Large Down Payment

Is a bigger down payment always better? Not necessarily. Here are some things to consider before you put down a high down payment on a potential house:

- You may not be able to afford it. Putting together a large down payment is not an easy feat on a typical household budget. It takes a lot of time to save 20 percent of a typical home’s purchase price. This may leave you out of the market to buy a home if you wait long enough. By the time you save up, it may not be enough of a down payment for the same type of home you wanted. It may be worthwhile to choose a smaller down payment amount in order to be able to buy your first home.

- It may not be necessary. Down payment requirements vary depending on the type of mortgage you get.If you are a veteran, VA loans require no money down. Even if you can’t get a VA loan, an FHA loan may still make it possible to get a home with as little as 3.5 percent down. If you are like many first-time homebuyers, it may make more financial sense to use a VA loan or FHA loan and pay a smaller down payment so that you actually get your foot in the door.

- Less budget flexibility. A high down payment may be great for your home, but what happens if you lose your job? That’s what often happened during the economic crisis of 2008, and it led to many foreclosures. A larger down payment is not worth risking an empty savings account, or worse, an empty investment account. It’s important to be able to maintain cash reserves for an emergency fund in case of unexpected expenses.

- Retirement issues. If you are taking out a 401(k) loan, then you may have a hard time once your retirement hits. Too much investment removed can end up harming your retirement fund later on in life.

Average Down Payment on a House

The average down payment amount people actually make on a house may be smaller than you think. Did you think that most people put 20 percent down or more? You are not alone, but that’s far from the truth. The NAR reports that the median down payment was well under that figure at 14% in 2023.

Age is a factor in how much of a down payment people have. Younger home buyers typically pay smaller down payments. For people under 30, the typical down payment for a home is only 8 percent of the asking price. People above the age of 65 typically put down 20 percent or more.

There are different ways to calculate your down payment, so it’s good to read up on which method you should expect to use.

Average Down Payment on a House for a First-Time Buyer

The average down payment on a house for a first-time buyer is only 6 percent. Shocked? Many people are. It’s easy to see where first-time homebuyers may be concerned about being unable to buy a home due to issues with down payments.

Part of the reasons for such a surprisingly low down payment are the many loans and programs geared towards first-time homeownership. New buyers are often still getting their financial footing underway, so the government does what it can to ensure new buyers aren’t priced out of the market.

Once they build equity, they can generally use that home equity to purchase their next house with a higher down payment.

Minimum Down Payment on a House for a First-Time Buyer

The minimum down payment on a house for a first-time buyer can be zero. However, the true minimum you can put down depends on which program you use to get a home. Only a handful of financing programs allow for a zero down mortgage.

The United States tries to be amenable to first-time homebuyers who are either veterans or are looking into buying rural homes. VA loans and USDA allow you to get a home with no money down, while FHA loans offer you the opportunity of homeownership via a 3.5 percent down payment.

VA loans are known for being available exclusively to veterans, while USDA loans are only for people who want to buy in rural (or sometimes suburban) regions. FHA loans, however, are generally open for almost anyone who is buying a house for the first time.

The minimum down payment for a first-time home depends on the type of loan programs or alternative financing programs available to you. Here’s a quick run-through of the most common types of loan programs:

- FHA Loans: 3.5 percent. By and large, the most popular way to afford a first-time home, FHA loans are an excellent choice for people who want to have a lower down payment but can’t quite qualify for a HomeReady or USDA loan.

- VA and USDA Loans: 0 percent. Veteran loans and USDA-approved home loans can be done with no money down. USDA loans can be obtained by low and moderate-income families who want to move to approved areas.

- HomeReady/Home Possible: 3 percent. Certain Fannie Mae and Freddie Mac programs, such as HomeReady and Home Possible, can allow you to get a home with 3 percent down.

- Conventional Loans: 20 percent. A conventional loan, also known as a traditional loan, typically requires a minimum of 20 percent in most situations.

It’s important to note that putting the minimum down is not always the best idea. Most of the time, the minimum is a starting point for figuring out the best down payment for your financial situation—not the ideal amount to offer.

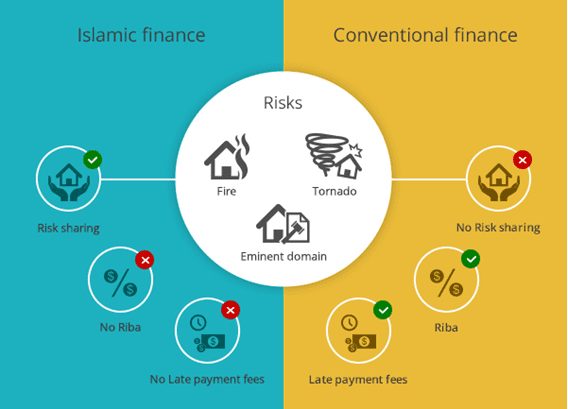

How Does This Apply to Islamic Financing With Guidance Residential?

As the #1 U.S. provider of Islamic home financing, Guidance Residential does not offer mortgage loans — our contracts are based on a different foundation that is free of riba, or interest.

Still, we can offer much the same flexibility as more conventional loan programs. In some circumstances, we are able to offer Islamic mortgages with as little as 3.5% down.

Speak with your Account Executive for more information on what is available to you.

Consider Other Costs When Deciding on the Right Down Payment

When deciding on the right down payment for your situation, remember that a down payment isn’t the only payment you will have to make at the time of your home purchase.

In addition to the down payment, there are several other upfront costs associated with buying a home. One significant expense is closing costs, which typically range between 2% and 5% of the loan amount. These costs encompass a variety of fees, including loan origination fees charged by the lender for processing the loan, appraisal fees to assess the value of the property, credit report fees, and fees for conducting title search and insurance that protects the lender and owner against legal issues with the property title.

Closing costs also cover escrow deposit for property taxes and mortgage insurance, if your down payment is less than 20% of the home price. Some buyers also choose to pay points, a type of prepaid interest, to lower their mortgage interest rate and therefore their monthly mortgage payment amount.

Home inspections, which are essential to identify potential issues with the property, represent another cost. Furthermore, homeowners insurance premiums and potentially private mortgage insurance premiums (if your down payment is less than 20%) add to the expenses.

Lastly, moving expenses and immediate home repairs or upgrades are often necessary costs that can be significant but are sometimes overlooked by homebuyers. It’s crucial for prospective homeowners to leave enough money to cover these additional costs when deciding on a down payment.

The Bottom Line: Should I Put a Large Down Payment on a House?

Is a larger down payment better? It really depends on you and your situation. If you can comfortably afford to get a substantial down payment, then it could prove to be a smart move—especially in a hot market.

However, if you are struggling with money and want to own a home, it may not always be possible to do so. This is why most guides that involve deciding how to choose your down payment tend to leave some leeway. It’s not always realistic to continue to wait and save.

When in doubt, it’s best to shoot for a larger down payment. If that’s not always doable, working with a down payment that’s close to the national average will usually suffice.

Find out how much home you can afford today with our handy affordability calculator. To get a more accurate estimate, complete the online pre-qualification process with Guidance Residential. It takes fewer than 10 minutes from start to finish. Check it out now.

Originally published July 2020, updated December 2023.