Homebuyer Webinar Recap, April 4, 2026

“Understanding and Avoiding Riba-Based Banking Methods”

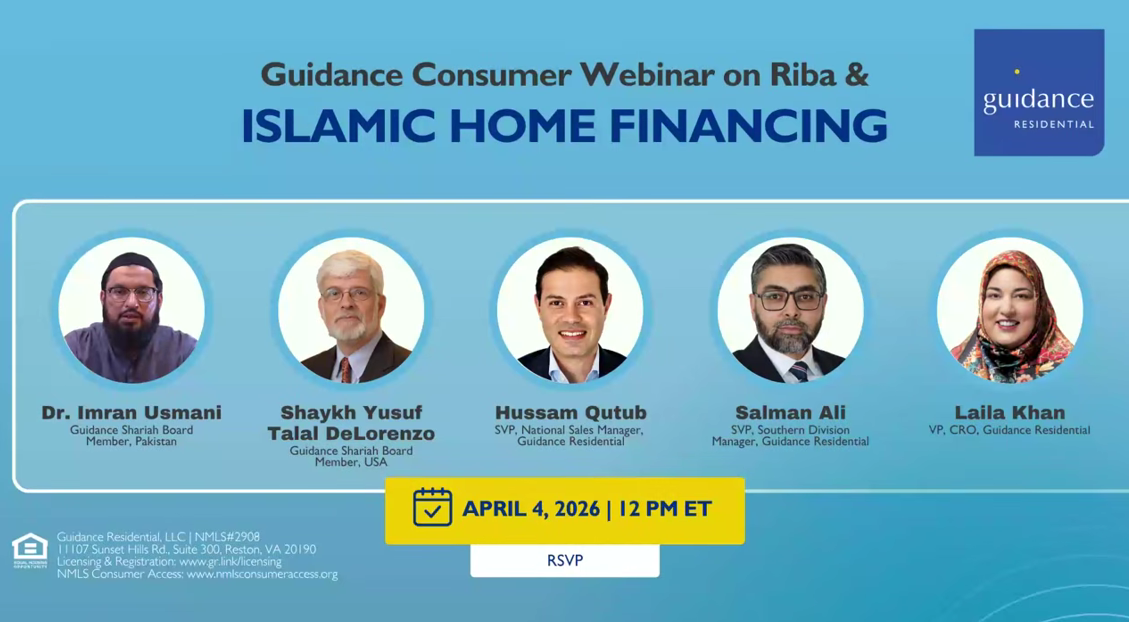

Event date: April 4, 2026

Featuring Shariah Board members Shaykh Yusuf Talal DeLorenzo and Dr. Imran Usmani, with Guidance leaders Hussam Qutub (SVP, National Sales) and Salman Ali (SVP, Southern Sales Division). Hosted by Laila Khan, VP of Community Relations & Outreach.

Watch the Recording

Webinar Summary

On April 4, 2026, Guidance Residential hosted a national webinar, “Understanding and Avoiding Riba-Based Banking Methods.” The panel featured Shariah Board members Shaykh Yusuf Talal DeLorenzo and Dr. Imran Usmani, alongside Guidance SVPs Hussam Qutub and Salman Ali. It was hosted by Laila Khan, VP of Community Relations and Outreach.

The session covered why Riba is prohibited in Islam, how Guidance’s Declining Balance Co-Ownership Program (diminishing Musharakah) works as a true alternative to a conventional mortgage, and how Guidance’s structure compares to other providers in the market. The panel closed with a live Q&A covering funding sources, provider comparisons, maintenance responsibilities, and profit rate benchmarking.

Key Takeaways

| Guidance Residential is not a bank. It is Muslim-owned and Muslim-led, with no ties to a conventional Riba-based bank or lender, so profits never flow back into interest-based banking. This is co-ownership, not a loan. Guidance and the homebuyer purchase the home together through a declining balance partnership (diminishing Musharakah), and the homebuyer’s ownership share grows with every payment. Guidance shares real risk with customers. Financing is non-recourse, late fees only cover actual administrative costs (never profit), and losses from events like natural disasters or eminent domain are split based on each partner’s ownership share at the time. Homebuyers keep 100% of the appreciation. Because customers use the entire home and are responsible for its maintenance and property taxes, they also receive the full benefit when the home’s value goes up. The profit rate is benchmarked to market rates for comparison, not because the contract works like a loan. Shariah permits using a market rate as a benchmark for a fair rental price. What makes financing halal is the underlying contract, not whether a number resembles an interest rate. An independent Shariah Supervisory Board oversees the program, including annual audits, to confirm the structure stays fully compliant over time. Guidance Residential has provided more than $10 billion in financing to more than 40,000 families over 25 years, with programs now available in 35+ states. |

Frequently Asked Questions

What is the source of the funds Guidance Residential uses to finance homes?

Guidance’s initial funding comes from Capital Guidance, the Muslim-owned private equity group that has funded Guidance’s research and development since inception. To scale beyond that initial capital, Guidance created a Shariah-compliant securitization structure, similar to a sukuk, and partnered with Freddie Mac and Fannie Mae, both congressionally chartered institutions, to bring in institutional investors as silent partners in its co-ownership agreements. Guidance also now offers everyday Muslim investors the opportunity to invest directly in these homes. Guidance remains the owner of each co-ownership LLC throughout.

How is Guidance Residential different from other companies offering Islamic home financing in the U.S.?

Many other “Islamic” home financing options are subsidiaries of conventional, Riba-based banks, which means profits ultimately flow back to interest-based institutions. Guidance Residential is independently Muslim-owned and Muslim-led, with no ties to a conventional bank. It is also one of the few providers using a true risk-sharing, diminishing Musharakah structure instead of simply relabeling a conventional loan. When comparing providers, ask who owns the company, whether it is affiliated with a Riba-based institution, and whether it genuinely shares risk with the homebuyer.

Does Guidance Residential share in home maintenance costs or property taxes?

No. Guidance’s program uses a joint ownership (shirkat al-milk) structure, not a joint venture, and the homebuyer has full use of the property from day one, regardless of ownership percentage. Because the homebuyer benefits from all appreciation in the home’s value and from the local services property taxes fund, they are also responsible for maintenance and taxes tied to that use. This follows a foundational Shariah principle: whoever uses and benefits from a property pays the costs of that use.

Why does Guidance Residential’s profit rate look similar to an interest rate?

Guidance benchmarks its usage fee against prevailing market rates so customers can compare costs fairly against conventional financing. AAOIFI’s Shariah standards permit using an interest-rate benchmark as a scale for setting a fair rate that is competitive in the market. This is not the same as charging interest.

Full Transcript

TRANSCRIPT: Understanding and Avoiding Riba-Based Banking Methods

Guidance Residential National Home Buying Islamic Finance Digital Event

Hosted by Laila Khan, VP of Community Relations & Outreach

Featuring: Shaykh Yusuf Talal DeLorenzo & Dr. Imran Usmani (Shariah Board Members)

Also Featuring: Hussam Qutub (SVP, National Sales Manager) & Salman Ali (SVP, Southern Division)

LAILA KHAN

Assalamu Alaykum and welcome to our national home buying Islamic finance digital event — our webinar: Understanding and Avoiding Riba-Based Banking Methods. MashaAllah, I’m here in DC, joined with colleagues all over the country, in Houston. We have our panelist speakers Shaykh Yusuf Talal DeLorenzo from Florida and our very esteemed Honorable Dr. Imran Usmani from Pakistan.

My name is Laila Khan. I am the Vice President and serve all community relations and outreach initiatives here at Guidance Residential. Alhamdulillah, I’ve been with the company for over 10 years in Islamic finance and in the national community space for over two decades. It’s a pleasure to be here and to welcome each and every one of you.

While I go over a brief overview of today’s program, go ahead and share with us where you’re dialing in from today — your city, state, and your name. We’re really looking forward to engaging with you. It’s 12:00 p.m. Eastern Standard Time for us. Morning for some of you. Alhamdulillah.

Today’s program: we’re going to go over who we are and a brief introduction on Guidance, why Islamic finance matters, how Islamic finance is different, understanding Musharakah, and of course my favorite part of all of our sessions — our live Q&A. We have a special treat: not only are we with our colleagues, but we have our esteemed scholars with us today to address all of your questions, InshaAllah.

Riba, which is lending and borrowing with interest, is prohibited in several verses of the Quran and the Hadith. For Muslim Americans, it’s imperative for us to avoid Riba when making what will likely be the largest purchase of our lives — our homes and our investment.

Islamic finance works to establish a fair and balanced approach in financial dealings where financiers establish real ownership and real loss sharing in every transaction. Over 25 years, alhamdulillah, Guidance Residential stands as the leading, number one U.S. provider of Islamic home financing. We are not a bank. Alhamdulillah. Most cannot say this. We are privately funded and privately owned. We work in Islamic finance with a very clear vision, and over the years the institution has remained committed to building institutions and providing alternatives to the conventional financial systems.

I’m joined by my two dear colleagues: Hussam Qutub, our Senior Vice President of National Sales Manager, and Salman Ali, also a Senior Vice President and manager of our Southern Sales Division.

Dr. Imran Usmani is our Shariah board member here at Guidance Residential. He is a highly respected Islamic finance scholar who has served as an adviser and member of independent Shariah boards of several renowned institutions since 1997, including the State Bank of Pakistan, Guidance Financial Group, and many others. He has also served as an executive committee member of AAOIFI, the world’s leading nonprofit institution responsible for the development and issuance of standards for the global Islamic finance industry.

Shaykh Yusuf Talal DeLorenzo is also a Shariah board member with Guidance. He is considered a leading authority on Islamic finance in the United States. Over 20 books have been translated from Arabic, Persian, and Urdu for publication, including the three-volume compendium of legal rulings on the operations of Islamic banks.

I’d like to give the floor to you both to share a few words.

DR. IMRAN USMANI

It is really a great honor to be here with you. In Pakistan it is 9:00 p.m. Thank you very much for arranging this webinar. I hope and trust and believe that InshaAllah it will be very useful and productive and will resolve many questions you have in your mind. Please feel free to ask any question and InshaAllah we’ll try to reply to all of them.

SHAYKH YUSUF TALAL DELORENZO

It’s a pleasure to be with you here today. I hope that we can provide some answers to the questions you may have in your mind. We appreciate your coming out at this time of day and look forward to talking to you. It’s always a learning experience for us to interact with people who have genuine questions — not theoretical but practical. That makes a difference not only to you but to us as well. We appreciate it and look forward to speaking to you about whatever is on your mind with regard to Shariah finance. Thank you.

HUSSAM QUTUB

Thank you, Laila. Welcome everyone. It is a true pleasure to be with you this Saturday. We know it’s a day where you spend time with family, but I think this topic absolutely rises to the occasion, especially for Muslim Americans. We are thrilled and honored that two of our Shariah board scholars — two of what would be considered renowned scholars in the world in Islamic financial transaction laws — have made the time to join us in this discussion.

It’s a real treat for our audience here in the U.S., because it’s not every day that we’re able to ask Dr. Imran Usmani to spend time with us during his evening hours — 9:00 p.m. in Pakistan — and Shaykh Yusuf, of course, with his busy schedule. Very, very excited about what we’ll be sharing with our audience today. I hope it is extremely beneficial for all who intend to live their lives in accordance with Islamic financial transaction laws when dealing in the topic of home ownership, refinancing, and such things.

SALMAN ALI

Salam, everyone. It’s a pleasure to be here. Very, very excited. This is a once-in-a-lifetime opportunity. InshaAllah you’re going to learn a lot about Guidance Residential, learn about our program, and hear from these amazing, very knowledgeable, and respected scholars. I see a lot of questions coming in the Q&A box — keep them coming, InshaAllah. We’re intentionally saving them until the end. So if we’re not answering your questions right now, don’t get disheartened. We’re monitoring them. Keep them coming and we will have a live Q&A session at the end. Thank you everyone for joining.

LAILA KHAN

Thank you so much, Salman. We’re going to start our program with who we are and introducing Guidance Residential. As I mentioned, mashallah, we are approaching our 25th year. It’s hard to believe how time flies, mashallah, and we’ve remained committed and consistent with our offerings and our services.

HUSSAM QUTUB

For those of you on this webinar today who have never heard of us — you’re going to learn something that I think is going to be truly reassuring for you and your family. This year is 24 years in live operations, meaning serving the community. It’ll be 25 years next year.

The work we’ve taken on began even earlier, and I’m going to try to cover a lot of that with you, because you should absolutely feel comfortable with the institution you’re engaging with. Who owns the institution? What is the institution about? These are important aspects of the journey to identify a pathway for your finances.

Guidance has been a household name for many, many Muslims across this country. We are a values-driven financial institution solely dedicated to providing solutions that adhere to Shariah principles. We have been the pioneer in this space, developing creative solutions for Muslim consumers at both the retail and institutional investor level for 25 years.

The institutional investor has been introduced to us dating back to 2002 across many markets outside of the United States — in the Middle East and in Asia. We are global. Here in the U.S., what most folks recognize is our home finance program that was launched in April of 2002. But we have created a leading Shariah-compliant home financing program also in Saudi Arabia, in Morocco, and in other places.

We began with home finance and have developed other programs and products across the financial spectrum. Investments is something we’ve also been very active in — developing unique Shariah-compliant investment vehicles around the world in liquidity investments, real estate, private equity, and industrial equipment.

One of the things that is crucial for everybody to understand is the fact that we are not a bank. We are not a subsidiary of a bank or any conventional Riba-based finance. We want to make that distinction because there are many options out there for American Muslims today. You’d be surprised to know that we are still the unique player in the market because of this fact — because we are not owned by a conventional Riba-based institution or a conventional bank. We built this entire operation from the ground up to be a fully Muslim-owned Islamic finance institution, completely independent from those other institutions.

SALMAN ALI

Thank you. Alhamdulillah, as Laila and Hussam have shared, everyone on this panel has been through this journey. It’s been nearly 25 years. Alhamdulillah.

In that time, Guidance Residential has become the number one Shariah-compliant home financing company that our community trusts and goes to for authentic home financing. Alhamdulillah, in nearly 25 years, we have financed over $10 billion worth of financing. We have over $4 billion in our servicing portfolio. We’ve helped over 40,000 — the number is around 45,000 — Muslim families in the United States. We are operational in 35 states, up from a humble beginning with just three. We have many local offices, local account executives on the ground to support our communities, and a staff of over 220 in the United States. Alhamdulillah.

The reason our American Muslim community chooses Guidance Residential is because of our authentic program. A lot went behind the scenes. We had a three-year, multi-million dollar research and development project that involved 18 law firms and six of the world’s leading scholars in Islamic finance — two of whom are with us today, alhamdulillah. Our goal was to align a Shariah-compliant home financing model with both U.S. and Islamic systems. After three years of R&D, alhamdulillah, we were able to develop a declining balance co-ownership program — a diminishing Musharakah — that establishes co-ownership between our customers and Guidance Residential.

HUSSAM QUTUB

This was an incredible undertaking. To spend three years and engage with 18 law firms that were very involved in the U.S. financial industry — this was a massive undertaking. I know Shaykh Yusuf was a part of it. Dr. Imran was a part of it. I’d love to hear from both of you about what you recall from that time.

SHAYKH YUSUF TALAL DELORENZO

Sure. I was contacted early — I think it was 1998. Prior to that time I had been working with a group that was not successful. They attempted to offer home finance without interest but thought it was just unfeasible. I know of other attempts that had been made on a very small scale, requiring 60% or 80% down and requiring people to wait in line for years before receiving financing.

The idea of developing a program that would be financially feasible for both consumers and for the business itself seemed to be impossible. And so along came Guidance, with determination that they would manage this somehow. They gathered a number of scholars. We met over two or three years of the development process here in the U.S., in London, and in Dubai. A lot of ideas were exchanged.

Most importantly, the law firms that joined us — particularly those with specializations in home finance and mortgages — were at first skeptical. But once they got to know us and listened to the ideas we were exchanging, they became very, very interested.

From a Shariah perspective we had several different solutions. The real challenge was to select one that would fit seamlessly within the systems here in the United States — systems plural, because obviously from state to state you have different requirements for the purchase of homes. We had to noodle our way through all of the details in all of the states. Of course we began only with a handful, but now we’ve moved on to 35 states.

HUSSAM QUTUB

We have seen as an institution the challenge of going into each one of those states — being licensed, getting the authorities to understand our structure and approve us to function. It’s a lot of heavy lifting. Dr. Imran, you were a part of this as well. I’d love to hear your perspective.

DR. IMRAN USMANI

Yes, sure. As I remember, I graduated from Jamia Uloom Karachi in 1988, then did my specialization in Islamic finance — my thesis in the third year was on Musharakah and the sale and purchase law in Islam. By that time, I joined in 1994 with an Islamic finance institution based in Bahrain.

Then I was offered to work in Malaysia with Dr. Sanaita Hashim, who was then the director of Guidance Financial Group, and I worked with her to develop an Islamic multimedia directory or database for Islamic finance and the islamiq.com website as editor, writing different articles and Q&A sessions.

We continued and then met with Dr. Hammour in 2000 in Geneva at a conference. He invited me to work with them — and Dr. Sanaita as well — to start this home financing program. In my thesis and then in my PhD, I discussed in complete detail how house financing could be based on diminishing Musharakah. On that basis, alhamdulillah, we were the first through Guidance to initiate the diminishing Musharakah program.

Alhamdulillah, later we saw it was very successful in all states while complying with all regulations. And once we launched that, we then launched in Pakistan — Al-Meezan Investment Bank, and then in 2001 or 2002, Meezan Commercial Bank — on the same basis of the declining co-ownership, also called diminishing Musharakah.

Alhamdulillah it is a very successful program and I’m feeling very humbled to have been part of it from the very inception. I learned from great scholars, especially my honorable father, who was with them for the whole journey, and some scholars who have passed away, like Dr. Abu Sattar Abu Ghuddah, who was also a member. We remember them with gratitude. And now it is a success story — mashallah, you have crossed $11 billion. Alhamdulillah. It is a blessing from Allah subhanahu wa ta’ala who has given acceptance among the people.

HUSSAM QUTUB

We all appreciate the blessings we’ve received. The effort was remarkable and led to many other things — not just here in the United States with our Islamic home financing Musharakah structure, but also to many other investment products that were the first of their kind.

One new program just launched is the Guidance Short-Term Income Trust here in the United States — just a few months old. It’s the first Shariah-compliant investment product in the United States for Muslims to put their money into something akin to a savings account. Muslims can now put their money in a Guidance Short-Term Income Trust — an Islamic income trust that provides liquidity and a return. The return comes from investing those dollars into our Musharakah structure, from the real estate we co-own with all of our customers. Go to guidanceinvestments.com to learn more.

Now, this is the Shariah supervisory board that was involved early on and is still involved today. Justice Mufti Muhammad Taqi Usmani still serves with AAOIFI as the chairman of that Shariah board — the leading standard-setting body for Islamic finance on a global scale. Their standards require any Islamic institution to have an independent Shariah supervisory board to oversee and approve all of its activities.

We want to clarify: this is still the independent supervisory board of Guidance Financial Group / Guidance Residential. Everything that occurs with the company must be approved from a Shariah perspective by these honorable scholars. Dr. Imran, maybe I’ll go back to you to reassure the public about the participation of yourself and your father in our independent Shariah supervisory board.

DR. IMRAN USMANI

If there is a misconception, it is completely wrong. My father is quite active still. As you mentioned, they have recently started an investment program so that Muslim investors could invest in the housing mortgage program through Islamic modes. My honorable father was actively involved and engaged in the structuring of it. I was witness because I worked with Dr. Hammour and the other team members on how to develop and structure that. We showed it to my father, he made some changes, and then there were several meetings with him, with Dr. Hammour, and with the team members of Guidance Financial Group.

I will assure you that my father is alhamdulillah still quite active. His vision is that in the United States, Muslims could get a Shariah-compliant and halal mortgage and also invest in Shariah-compliant investments. For that reason, he is quite active in this initiative as well. Alhamdulillah.

HUSSAM QUTUB

Thank you for that, Dr. Imran. We even have annual audits conducted. Shaykh Yusuf, you’re going to be conducting another one this year. Could you shed a little light on that?

SHAYKH YUSUF TALAL DELORENZO

Yes, InshaAllah. It’s a regular occurrence. I work closely with the internal legal department of Guidance Residential and have since the inception. We’re quite familiar with one another. We communicate by phone and by email. Questions come up and whenever they do, we get together and talk about them. I’m also the coordinator for the Shariah board.

When I go up for the audit, I prepare a report that is presented to the Shariah board at our next meeting. We meet regularly. So our eyes are continually on the goings-on at Guidance Residential, and we’re very, very happy with what we see. As an independent Shariah board, if we see something, it’s our responsibility to say something. This is part of any business operation, and certainly with regard to compliance with Shariah norms.

In the early days, we had a clear mandate from Guidance: find a solution, but one that complied in every step of the way with the precepts of Shariah. There were to be no shortcuts. We were to find a way that actually worked. And mashallah, it appears that this has been quite a success.

HUSSAM QUTUB

I will always say: this was one remarkable effort. I don’t really see anything like it here in the U.S. that took shape over those three years. Justice Muhammad Taqi Usmani still serves with AAOIFI as the chairman of that Shariah board. I have yet to see an institution with as many reputable, esteemed scholars as Guidance has on its independent supervisory board. That just goes to show the extraordinary steps we took to ensure that everything is done properly.

Speaking of Riba — every Muslim understands the prohibition, understands the severity, understands that we must do everything in our power to avoid a transaction with Riba. There’s a verse in Surah Al-Baqarah where it says, “They say that commerce is just like interest, but Allah has made commerce lawful and has forbidden interest.” You should feel reassured about this. Even during the time of the Prophet, sallallahu alaihi wasallam, there were people that still didn’t understand the difference between commerce and Riba. That made it into the Quran itself.

I’d like to give our esteemed scholars time to talk a little bit about Riba and share for our audience not just that it’s prohibited, but how it’s formulated. Shaykh Yusuf, I’ll start with you.

SHAYKH YUSUF TALAL DELORENZO

Sure. Abu Hurairah, one of the companions of the Prophet, reported that the Prophet said: “A time will come to people when no one will remain except those who consume Riba. And if they don’t directly participate in Riba, they will feel its effects.”

The wording was: if they don’t consume it themselves. It’s like a fire. You all know the statement that where there’s smoke, there’s fire. Riba, if you consider it to be fire, also has smoke. If you’re not burnt directly by the fire itself, we’re living in a time when we certainly are affected by the smoke — those continuing effects like waves going out from it. This is so obvious today. Everything that we do, all of our activities in one way or another are affected by Riba.

We live in the United States. We pay taxes. We subsidize through our taxes projects that are based on Riba. Our municipalities offer investments in public works also based on Riba — whether it’s the school, the police, the library, the roads. Now, we’re not paying out Riba for this. We’re not accepting it, but it’s a part of our society.

When we look at economic indicators, what are those based on? They’re based on interest rates, the Dow Jones, the 30-year Treasury. So Riba is a part of our society. And yet, mashallah, we are able to avoid it by certain strategies that we accept for ourselves and our families. One of the most important has to do with the financing of our homes.

It’s possible to finance a car on a zero-interest loan. It’s possible to buy a car outright. But very few of us are able to purchase a home outright, especially nowadays. So to have the opportunity through a reliable, long-standing financial institution such as Guidance Residential — that’s really a blessing from Allah.

HUSSAM QUTUB

There was a paper written by Justice Usmani that gave advice to the World Economic Forum on this subject — on the heels of the financial crisis between 2007 and 2009. It’s called “Post-Crisis Reforms: Some Points to Ponder.” We have that paper in the control panel for our audience to download. Dr. Imran, if you want to talk a little bit about that?

DR. IMRAN USMANI

Mashallah, my father has contributed so many books in different subjects. One very famous one is called “Historic Judgment on Riba,” which he gave during his time as a justice on the Supreme Court of Pakistan in the Shariat Appellate Bench. He gave a remarkable judgment that financial interest is considered as Riba. I would recommend all the audience read it — it’s available as a PDF. I have also translated that book into Urdu.

My father has also written another book, “Introduction to Islamic Finance.” And I have also written my own book which is taught in different universities and talks about the different practical aspects of how we can avoid Riba and how we can implement Islamic finance.

One thing I would mention: in the Quranic verse you referenced, the disbelievers said that commerce is very similar to Riba. Allah subhanahu wa ta’ala didn’t mention the rationale for why Riba is not allowed and commerce is allowed. He is the Almighty God; He does not need to provide any proof or rationale. He simply said: Riba is not allowed and commerce is allowed.

In commerce, if you are selling something at a deferred price, the price and the installments are fixed. If you lend money on the same basis — in installments — it looks similar. This is why the disbelievers made that claim. But Allah says: if you are selling a thing on credit, where the price is fixed and paid in installments, it is completely halal. But if you are giving a loan to someone and asking a premium above and beyond the principal amount, that is Riba. This is very clear, and every Islamic academy has unanimously said that commercial interest is not allowed.

As for the 2008 financial crisis — my father wrote a detailed thesis on this. Islamic finance was much less affected because it is asset-based, while conventional banking is not. For example, if you give a loan on a 5% or 20% margin and then sell that loan to someone — and they sell it again — you can create a bubble from very small margins that can erupt at any time. But in Islamic finance, you have to have the actual asset behind the whole house and participate in its activity. There is no such bubble. And if you securitize those certificates — as we are doing through Fannie Mae or Freddie Mac — it is based on sukuk representing real assets, not just numbers or loans.

This is the basic difference: Islamic finance is always completely backed by particular assets or services. There are no such loss chances from speculative transactions.

HUSSAM QUTUB

We’re going to share some visuals with the audience to help take something complex and simplify it. One quick way to simplify this: lending money is a charitable activity, not meant for commerce. Lending and borrowing is really to assist those experiencing hardship. The loan agreement is not meant for commerce, investment, or trade — it’s meant only to assist those in hardship.

So what are the agreements that can help facilitate investment? Purchasing a home is an investment. What type of agreement is a halal agreement? We’re going to get into a lot of that today.

First, let’s talk about the ramifications of Riba. Salman, we talk about this all the time — living in this world, we get to see some of the ramifications up close and personal.

SALMAN ALI

Exactly, and even more so today. Why does Islamic finance matter today more than ever?

When we look around the world, we see rising inequality, rising debt, rising poverty, and rising unemployment. Just to break it down: 10 billionaires have more wealth accumulated amongst themselves than the poorest half of the world. Subhan Allah. 30,000 children under the age of five die every day — due to debt, according to UNICEF. In the United States, the richest country in the world, nearly 650,000 people are homeless and nearly 37 million people — 11% of the population — live in poverty. 13.5% of U.S. households were food insecure. Subhan Allah. And globally, an estimated 210 million people are unemployed.

Subhan Allah, when we really break it down, it comes down to debt and the current financial and banking system.

HUSSAM QUTUB

The current modern economic system is what we believe is behind all of this rising inequality, debt, poverty, and unemployment. We could spend an entire day on the next few slides — we’re not going to do that. But the entire modern economic system is built around fractional reserve banking, grounded in a value-neutral economic philosophy, creating a debt-based economy. The process that keeps it growing involves lobbying, speculation, deregulation, and ultimately exploitation.

I’d really encourage attendees to take a screenshot of this slide, because this is important for every single person to have awareness of in terms of their financial affairs.

The root cause: many consumers just don’t recognize that money in our economy today is created by banks in the form of bank deposits. The modern system of money creation in the U.S. Federal Reserve system really gets its energy from the relationship between us as individuals and commercial banks. We deposit money into banks, which acts as the fuel for a fractional reserve multiplier.

Here’s how it works, in simple language: We have money that we earn — hopefully in a halal way. We deposit it into a bank for safekeeping. Let’s take a $1,000 deposit. The bank reserves 10% — $100 — and loans out 90%, which is $900, at interest.

A consumer comes along and spends that $900 — let’s say, buying an airline ticket. The airline receives that $900 and deposits it into their bank account. That $900 enters the bank. The bank reserves 10% of it ($90) and loans out $810. That consumer spends the $810, and the cycle continues.

Just after three of these cycles, $1,000 that we deposit in the bank becomes $3,439 in the system.

There are two problems here. One: our money is being weaponized for Riba. Our money is being put into the bank, and the bank is weaponizing it for the creation of Riba — without us clearly participating, even if we request a non-interest-bearing checking account. Two: we don’t know who they’re loaning it to. It could be things and activities we wouldn’t agree with — but we’re indirectly funding them.

This is the root problem: fractional reserve banking. What it does is create wealth out of thin air. The fictional financial economy is over 26 times larger than everything else produced on planet Earth. The system transfers income and wealth from the 90% to the 10%, where the 10% are net receivers of bank interest and the 90% are net payers. This is the inequality we were speaking of earlier.

So having described that world of lending and borrowing money at interest — what is the solution?

Well, let’s start with values. The system I just described runs on a value-neutral philosophy where the only values are tied to profits. If something can make money, it’s part of the value system. And if it’s illegal and makes money, that system works to deregulate it. Today, many of you as American Muslims know that there was a time you couldn’t gamble on your smartphone. Today, it’s been deregulated. Sports betting on your mobile device is now legal.

And there’s a level of deception that tries to make it seem like it’s not corrosive, not destructive — “it’s up to you to handle your own desires.” But then what do we see? We see instability. The booms and the busts. If you’re looking at finance that way, you’re never going to have a north star.

But Islamic finance as a solution establishes timeless values. They cannot be deregulated. There is regulation that’s good for mankind across the globe. There’s transparency. There’s stability as a result. It is a system that has foundational principles.

Shaykh Yusuf, you do a great job of helping the average Muslim understand these things. Can you speak a little bit about this?

SHAYKH YUSUF TALAL DELORENZO

Yes, indeed. Everyone knows that Islam has a very well-developed system of law and ethics called the Shariah. We also understand that the Shariah is relevant — or can be made relevant — to all times and places. It’s the responsibility of Muslims to do so, to understand their surroundings in the context of the eternal principles elaborated in divine law through the Quran, through the Hadith, through the practice of the sahaba and so on.

The interesting thing about Shariah is that it’s endowed with an internal mechanism for understanding and interpreting called ijtihad. It’s the responsibility of Muslims from every generation and in every place to practice ijtihad so that the eternal principles of Islam are interpreted in ways that make sense to the surroundings of Muslims wherever they may be.

With regard to finance, Allah has set down certain principles. Hussam mentioned one: the business of lending — lending is not business at all. Lending is a charitable act. When we make a loan to someone, we do so in anticipation of one thing only: reward in the next world from Allah, or possibly reward in this world. But we don’t expect to be necessarily paid back. It’s friendship. It’s charity. It’s family. It’s not business.

And why is it not business? We understand money to represent value, not to be value in and of itself. If I have a thousand rupee note or a $10 bill — from a Shariah perspective, that bill indicates to us an amount of value and nothing more. We can’t eat it. It’s not for consumption and it’s not for production. Money in and of itself is neither productive nor consumable. It’s simply an indicator. We can buy things with which to produce whatever we want — build factories, build whatever. Likewise, we can use money to purchase things. But we can’t use money to make more money out of money. That’s the problem.

Modern finance uses money like a commodity. It turns money into something that can be traded — and even the absence of money in the form of debt can be traded. So what’s being traded in modern finance is essentially nothing for nothing.

Islam insists on money as a measure of value, not value itself. Islam also insists on the sharing of risk, on transparency. When we deal with others, we’re to deal equitably. We’re not to traffic in the debt of others. A debt is an obligation. It can be transferred in certain ways, but to buy it and sell it and speculate on it — that’s problematic. We also have very strict rules about gambling. The fuqaha through the ages have explained differences between speculation, real business, and gambling. Today’s world is just full of gambling in every direction.

Hussam mentioned the important facts of fractional reserve banking. I urge you to Google it — there are examples and people talking about it on YouTube and through Google. But the long and short of it is that it’s inflationary. What does it do to our economy? It just blows it up. The numbers that the government gives about gross national product — how much of those numbers actually represent real economic activity, versus inflationary financial activity — is probably close to 90% for the latter. We are continually being deceived by numbers.

But if we stick to the foundational principles behind Islamic finance, if we understand that there is a real economy behind all of this, then we can see really what’s happening to this world. We consume the smoke of Riba. It blinds us to the real situation.

Is there a solution for the whole world? We’ve spoken about it. Justice Usmani stood up at Davos and gave his talk. Davos was interested at that time because they saw that Islamic investments hadn’t tanked the way other investments had. Islamic banks didn’t go bankrupt the way that the “too big to fail” banks did. There was a clear difference, and they wondered: what is the difference? We’ve explained it to them in seminars, in writings, in books and treatises. And yet they’re not listening, because they can make money for nothing. That’s the great enticement of this century and the centuries before.

When we smell that smoke, what can we do? We can stick to the principles of Shariah to the extent that we can. You as perhaps first-time homeowners potentially need to keep this in mind. You can make a solid beginning for yourselves and your family, and as an example for your neighbors. I know my own neighbors are interested in what kind of home financing I have. And it’s important — let’s get the word out. There is a very different system. There’s a very different way to run the world. And for centuries, Muslims were very successful at doing so. For you, the potential home buyer — please consider a Shariah-compliant investment into your and your family’s future.

HUSSAM QUTUB

Dr. Imran, I sometimes try to help the average individual learn this topic at a very basic level — where I say Islamic finance is really just investing, not lending. Would you share a brief overview?

DR. IMRAN USMANI

Let me share a brief theory so people could understand the actual difference. If I summarize everything, I can say there are two basic things: usul al-Shariah — the principles of Shariah — and maqasid al-Shariah — the objectives of Shariah.

If we go through all the resources of Shariah — the holy Quran, the Sunnah of the Prophet, qiyas (analogy), and ijma — we find three things that are allowed and on the contrary things that are not allowed.

The allowed things: sale of goods or services that have particular value as per Shariah. Those things not considered goods of value — like debt, interest, certain derivatives, certain options — are not goods or services and are not allowed to be sold.

The second usul: every transaction should be very transparent. It should not have any ambiguity that could lead to a dispute. One transaction should not be tied to another. It should not be contingent on an uncertain event. The subject matter should be well-qualified, well-quantified, well-defined. This is called transparency or gharar-free.

The third usul is called risk sharing. If you are going to invest somewhere, you should not put all risk on the other party — you should share it. In lending at interest, whether the borrower makes a profit or a loss, you have to be paid. But if you are making an investment through Mudaraba or Musharakah, you participate in the venture and share in the risk.

Those are the three usul al-Shariah. Now the maqasid al-Shariah — the objectives behind these principles — are: first, there should not be any injustice to anyone. In lending, there could be injustice, because maybe the borrower is very poor and has a need and you are charging extra. Second, the circulation of wealth should be on a fair basis. Islam says in the Quran that your wealth must not be concentrated in a few wealthy people. Third, you should not spread disruption, inequality, unfairness, or injustice in society. If you are selling things that are not lawful or not good for society — this is also not allowed.

So we have to take care of both usul al-Shariah and maqasid al-Shariah. As you mentioned: investing is a win-win framework — investment in real assets, risk is shared, fair, profit and loss sharing. On the other side, the lending framework: sale of debt, risk transferred to one side, unfair gain, rich get richer and poor get poorer. No equitable basis. This is the main thing. And this is the precise summary of whatever is allowed or not allowed.

HUSSAM QUTUB

Thank you so much, Dr. Imran. All of these were considered in the process we look back on between 1999 and 2002. It really came down to these three types of structures that were considered: the Murabaha contract, the Musharakah contract, and the Ijarah contract. I’d like to ask you both to give us some insights into why Musharakah was selected over, for example, Murabaha — which is becoming again an option in the U.S. for American Muslim consumers.

SHAYKH YUSUF TALAL DELORENZO

When we began discussions of possible ways to accomplish what Guidance had in mind, we looked at the building blocks of Shariah finance. We narrowed them down to three with regard to home purchases here in the United States. Then the debates began — not only between Shariah scholars amongst ourselves, but also with the business team and members of the legal teams. I should also mention the tax people — a very important fourth group.

When we discussed each possibility, we had advocates from among those groups for each of the three methods. What finally developed was the idea that we should go with the partnership model — not only because it’s an authentic, clearly understood mode of financing, but also because everyone understands partnership and equity financing. Equity partnerships in mortgages is something that’s even practiced here in the United States. The system is not completely alien. That was to its credit. And then of course the idea of Musharakah includes with it the idea of transparency — because what are partners if not clear with one another about what they’re doing, their goal, and how they’ll achieve it?

Musharakah made a great deal of sense. Once we decided on that particular model — and it took a while; there were some pretty heavy debates — the question came about which sort of Musharakah to adopt. In the traditional, classical body of Islamic law there are all kinds of Musharakah. We settled on discussions surrounding a declining balance sort of partnership.

Most people think of partnership as a joint venture. But the partnership Guidance settled on was actually not a joint venture type, but a joint ownership type — which we’re going to help everyone understand how it works.

DR. IMRAN USMANI

You can use Murabaha, you can use Musharakah, you can even use all of them in different places. But while choosing the best one for the United States, we selected Musharakah. Why not Murabaha?

There are two reasons. In Murabaha, the first reason is: Murabaha is a sale transaction in which you sell on a credit basis, and once you have sold, it becomes a debt — an obligation to pay a price. Debt cannot be resold; it cannot be securitized. If you want to make a sukuk out of that, it cannot become a sukuk to be traded in the secondary market.

The second reason is: in Murabaha, the installments are always fixed — they cannot be variable. For a 20-year or 10-year term, it would not be fair for either party to have a fixed rental or fixed price, because interest rates may go high or low. If rates go high and you’re charging a lower price, it’s not feasible for the bank to cover its cost of funding. And if rates go lower, the customer would say they can get a better price from another bank. So Murabaha is usually used in Islamic finance for short terms — 6 months, 3 months, 2 months — where a fixed price is feasible. For long-term it is not feasible, and it cannot be securitized.

The second option — Ijarah — is where the company would own the property and just charge a rental. The problem was that in the United States, with so many mortgage companies, if over 20 years you’re just paying rental and that mortgage company goes bankrupt, you could lose your property.

But in Musharakah, if you pay anything, it gets divided into two parts: one part is for acquiring the equity of that particular property, and the other part is rental. As soon as you have more and more equity in the property, your rental decreases. It is very flexible, very equitable, and it can also be securitized.

There are also two types of Musharakah: shirkah al-aqd (joint venture partnership) and shirkah al-milk (joint ownership). We selected shirkah al-milk. Why? Because in shirkah al-aqd, it is not allowed to buy out the other party’s shares at a pre-agreed price as per Shariah. While in shirkah al-milk, it is allowed — one partner can say: you can buy my share after a certain period at a particular pre-agreed price. This is the very good thing about Guidance’s structure — they say: I will sell my share to you, I will decrease my ownership, and sell to you at par value. Whether the price of the house goes high or low over 20 years, the customer has to give that particular face value for acquiring the equity or principal amount. And the remaining portion that Guidance owns — for using that portion, the customer pays a rental. As soon as the customer’s equity becomes more and more, the rental reduces according to the formula.

This is the whole concept, and it is completely allowed by the AAOIFI Shariah standards. I can show you this book — the AAOIFI Shariah Standards — in which it is completely allowed to use the diminishing Musharakah concept. And we have kept all rules and regulations in that particular contract complying to those standards. Alhamdulillah, it is a very workable, equitable, and flexible arrangement.

HUSSAM QUTUB

Alhamdulillah, this was very informative. Again, this is really the structure of shirkah al-milk that is of great benefit to American Muslim home buyers — because the appreciating value of that home goes back to the consumer. They still benefit from the property’s value increasing. Typically, over the course of five, six, seven years, properties in the U.S. increase. It is an investment after all. The benefit is that we don’t rob the American Muslim consumer from any increased value or appreciating value of the property.

Salman, can you walk us through the actual process as it compares to a conventional mortgage?

SALMAN ALI

Thank you. A lot of folks have been asking: how does the program work?

Our program is very simple. We don’t lend money. Instead, we create a co-ownership agreement and purchase the property with you. In four very simple steps:

Step 1: InshaAllah, you find your dream home. Our minimum down payment requirement is only 3%. We’ll put down the remaining 97% and purchase the property together as co-owners. The ownership of the property is determined by each party’s down payment.

Step 2: You make a monthly payment to Guidance. Part of that payment is a utility fee for using our share of the home, and the rest is a payment to increase your ownership in the property.

Step 3: As you make your monthly payments, Guidance’s ownership decreases while your ownership increases.

Step 4: The fun part — you eventually buy us out entirely and become 100% owner of the property.

What really makes us unique is that we’re a fully independent organization, disassociated from any banking activities. We’re not even a subsidiary of a bank. Alhamdulillah.

HUSSAM QUTUB

This is an important slide because it helps the public recognize the key benefits.

Benefit number one: pleasing Allah, abiding by His laws, avoiding Riba. Now that we understand we’re not becoming borrowers and the relationship is based on a co-ownership arrangement — not a lender agreement — what happens as a result of that arrangement?

First, on any late payments: there isn’t a penny of profit that Guidance makes on a late payment fee. We have a late payment fee that offsets only our administrative costs for reminding you if you happen to be late. We hired a research company just to tell us what the administrative cost is — the hard cost, even the cost of the stamp for sending out that reminder. What that came out to is about $50 in admin fees. That is what we can charge when someone’s late — to offset the administrative cost now burdened from reminding somebody to meet their obligation on time. That’s permissible.

What do conventional banks and mortgage companies do? They charge you a 5% late payment fee. If your monthly mortgage amount is $3,500, you’re going to pay a late fee of $175. That amount is profit. They actually profit when you’re late, which is not permissible Islamically. And it compounds each month.

Second: a non-recourse commitment. In the event, God forbid, that the customer defaults — months and months go by, even with forbearance plans in place, even perhaps a year or two — and the customer simply cannot get back on course. We then have to come to an understanding that we should probably liquidate the asset. We should sell it. And if there’s a shortfall in the proceeds, let’s say there’s a loss — for example, a $100,000 property where we’re 90% owners and the customer is 10% owner, but the house only sells for $80,000. We have non-recourse in every single contract in every single state. That means we would take a $10,000 loss and the customer would take a $10,000 loss.

In states where conventional recourse is allowed — which is most states in the United States — a conventional mortgage company would sell the house, recoup the $80,000, but then come after you for the difference. They would issue a deficiency judgment through the courts allowing them to garnish your wages, a car you may own, whatever you may have. This happened at record levels after the financial crisis of 2007-2008 — Americans gave their keys to the banks and walked away from their homes, and the banks chased them a year or two later with deficiency judgments. That is not permitted. We don’t have that in any of our contracts.

Third: true risk sharing. In cases where the customer is not the reason for dissolving the contract — in the case of natural disasters or public service projects where eminent domain is exercised — if proceeds coming from, say, the insurance company on a natural disaster are insufficient, we take those proceeds and divide them according to our ownership stake at the time. Losses are shared pro-rata.

In similar situations, some conventional — and even some quote-unquote Islamic — providers out there will take the proceeds from the insurance company, make themselves whole first, and if anything is left over, you get it. That is not a true pro-rata loss-sharing structure. In fact, I have not found a company operating under Islamic home financing in the United States that does what we do.

These things make the co-ownership commitment agreement of Guidance very different from many other institutions out there — conventional or otherwise. It’s what’s led to a lot of media outlets in the United States inquiring about our risk-sharing structure. We received more inquiry into our program in 2011-2012 after the crisis than at any other time in the history of our organization. Many articles featured our risk-sharing structure.

The leading trade magazine of the U.S. housing industry, Housing Wire, awarded Guidance in 2024 with their Vanguard Award — a very prestigious award in the U.S. housing industry for the impact our housing finance structure has on consumers across the U.S. We were also recipients of the RISE Award from Freddie Mac, issued for making an impact in an underserved community.

Alhamdulillah, for the past 24 years, we have become the largest corporate sponsors of Muslim American nonprofits in the United States. But we’ve also held true to the important aspects of our faith. The Islamic financial laws and principles have never been stronger here at our organization from day one until today. This now concludes our presentation — and I think the most important part is the question and answer coming up. Laila, I’ll turn it back over to you.

LAILA KHAN

What an insightful program full of value-added content. Again, to our dear Dr. Imran and Shaykh Yusuf — we are very fortunate to continue to benefit from your contributions. Even as a practitioner in this space for so long, I always learn something new. We all do. We have hundreds online with us and we’re very grateful for your time and engagement. We have over a hundred questions that have come through.

I wanted to start with this one question that has come up throughout the session:

Question: What is the source of the funds Guidance uses for home financing to purchase homes?

HUSSAM QUTUB

I’ll give a short answer. At the beginning of this presentation, we talked about how Guidance is owned by a private equity group called Capital Guidance. Three Muslim families started Capital Guidance 65 years ago, and this private equity group took it upon themselves to fund the research and development for Guidance and its Islamic financial products and services around the world. The initial funding for everything we do comes from us.

Now we have to scale. We had to create a securitization mechanism — essentially what’s equivalent to a sukuk — for the ability to take the money that we go in with you as a consumer to purchase that house, and continuously fund more homes. We don’t have unlimited funds. So securitization is important.

We were very fortunate to establish a relationship with securitization mechanisms such as Freddie Mac and Fannie Mae. These are institutions chartered by Congress. They are not banks. They are not lending institutions. They create the vehicle — the securitization vehicle — to allow institutional-level investors to invest in mortgages here in the United States.

We struck an arrangement with both of those institutions very early on to help us with the liquidity and scale of our Musharakah structures. We are still the partner in the arrangement — we are the owners of the LLC on the co-ownership commitment agreement, which doesn’t change. What we do is offer institutional investors the revenue being generated from our Musharakahs as a silent investor in the transaction. And as mentioned today, we’ve opened that up to individual consumer investors — Muslims — to actually invest with us in these homes. This is an incredible ecosystem of liquidity and investment dollars in the financing of these homes.

DR. IMRAN USMANI

You are completely right. Usually other banks have a parent bank or parent financial company. But here it is a private equity of Muslim entrepreneurs. I have a connection with them for more than two or three decades. I know them personally and mashallah my father is also very well connected. They are very committed Muslims with their own different ventures and good capital. They started with that, and then they created the securitization program — which is also a Shariah-compliant sukuk program. And now they have also recently developed the investment program in which individuals can also invest.

SHAYKH YUSUF TALAL DELORENZO

There’s another aspect to this: working with these semi-government authorities — Freddie and Fannie — actually ensures a certain degree of protection to the homeowner as well. Not only is it a conduit for liquidity from the outside, it’s also a method — it’s a backup, a kind of check for the consumer — because the conditions imposed by these institutions on the consumer are tried-and-true programs that have been running through the government’s sponsorship, which is then passed on to the consumer. This too needs to be taken into consideration.

LAILA KHAN

Thank you all for responding to that effectively. Another very common question:

Question: What is the difference between Guidance Residential and some of the other companies in the U.S. that are offering Islamic finance and Islamic home financing?

HUSSAM QUTUB

Many of these institutions that seem to be emerging tend to be subsidiaries of conventional regional Riba-based banks owned by non-Muslims, or conventional loan originators — types that are simply in the U.S. mortgage business with Riba being generated through and through. What we’re seeing is that they recognize there is a demand by American Muslims to stay true to their faith and participate only with institutions offering legitimate Islamic home financing. And when that happens, of course, the Riba-based institutions don’t want to be left out — they want to capitalize on the Muslim-American economy. So they offer these subsidiaries.

The problem is that these subsidiaries are owned by those institutions, so profits ultimately go back to funding conventional Riba-based financing structures. When you’re looking at competitors, ask yourself: who owns this institution? And is that institution completely opposite of what I’m trying to achieve — avoiding Riba? Is it an institution that’s propagating Riba?

And then absolutely look at the structure — because the structure is important. I haven’t yet seen a structure that does true risk sharing at the level of a diminishing Musharakah. Those are questions I would ask if I were a consumer in this space.

SALMAN ALI

You covered it really well, Hussam. And it really just comes down to these core questions that the Muslim community — especially in the last few years — has become especially aware of: how we spend our money, where we spend our money. We’re voting with our wallets. Even in something like coffee, we decided not to go to a certain coffee place and instead support Muslim coffee owners. As a result, something beautiful happened — we have all these Muslim-owned coffee shops, and it comes back to that Muslim circular economy.

If we did the same with financial institutions — the checklist: Is it Muslim owned? Is it a conventional bank? Is it Muslim managed? Do they create a true co-ownership agreement? Is Islamic financing their core business? Are they involved in any Riba business dealings? Do they share in the loss in case of natural disaster, eminent domain, and foreclosure? And most importantly: does the Muslim wealth stay within the Muslim community through that circular economy?

LAILA KHAN

These are great points and very common questions we’ve been coming across. I’m going to go to the next question:

Question: Does Guidance share in the maintenance of the home, and if not, why not?

HUSSAM QUTUB

We use a shirtat al-milk structure — a joint ownership structure — not a joint venture structure. The purpose is for transferring ownership and all the benefits to the consumer. From day one, the benefit to the consumer is that they have full occupancy of the home, even though they may be 3% or 5% owners, and they benefit from all the local services and from the appreciating value of the property.

They benefit from every penny of appreciation the property can endure over time. We don’t benefit from that. We only charge for usage of our portion of the property. We benchmark the cost of what it would be to use our portion of the property while you’re buying us out. So when you maintain the property as the person occupying it, every dollar that goes into maintenance actually helps the appreciating value of the property — and that benefits the occupant, not Guidance. Therefore we don’t share in the maintenance cost or the tax cost, because those taxes go to supporting the occupant’s needs from a jurisdiction perspective — public schools, roads, local law enforcement. And if those services are done correctly, values increase — and again, who benefits from that increase? Solely the customer.

If it were a joint venture, yes, we would think about splitting expenses according to our ownership percentages. But that’s not what this type of partnership is about. I’ll defer to Shaykh Yusuf or Dr. Imran to add.

SHAYKH YUSUF TALAL DELORENZO

You’ve explained it very succinctly. We might add the fact that the choice of the property was the consumer’s. You as the prospective homebuyer — you choose the property based on your perceived needs. You want to be in a really good school district, a quiet neighborhood, near the ocean, near an international airport, whatever the case may be. Guidance is totally neutral about all of that. And so if your choice results in higher taxes or in higher costs for this, that, or the other thing — that’s a result of your choices.

DR. IMRAN USMANI

Let me add something crucial: every step in this Guidance program, the user of the property is the client. Guidance is just an owner — whether it owns 1% or 90%. But the usage of the property is entirely with the customer. This is why we have signed another contract with them: the leasing contract, to use that property and pay a rental.

From day one, even if the client has very little equity in the ownership, 100% of the usage is done by the client. And ultimately, once he owns the property completely, he is the owner and the user.

The principle of Shariah is: whoever uses a particular thing and pays the rental should pay the normal maintenance charges of that. For example, if I own a car and give it on a lease to someone for a month, a year, or 10 years, all expenses related to their usage are borne by the lessee. Same thing here — the client is the co-owner as well as the one using the whole property. Because of using the whole property, he should pay all expenses related to the property’s maintenance and all taxes related to that.

HUSSAM QUTUB

Thank you, Dr. Imran and Shaykh Yusuf. One thing we didn’t mention: at any point, if it’s a 30-year term, the customer has the right to buy us out with no penalty. The client has control of that. They can end the Musharakah structure in two years if they choose — buy us out, and the home is 100% owned by the customer. The customer gets a lot of rights in this arrangement, and we’re really here to help facilitate full ownership of that home for that customer, without taking away the real, tangible financial benefits that are afforded to homeowners across the country who own real estate.

LAILA KHAN

Thank you so much. I also want to share that there are a number of questions specific to pricing and individual interests. I’d like to refer you to our website and the QR code on screen. One of our licensed account executives will reach out to you and review your details, facilitate your next steps in Islamic home financing, and answer those specific questions.

We’ve gone a little beyond schedule, so I’ll share just one or two more questions in respect of everyone’s time.

Question: Why does Guidance benchmark profit rates with interest rates?

Shaykh Yusuf, would you like to go first?

SHAYKH YUSUF TALAL DELORENZO

The interest rates published every day provide the market of home buyers with a benchmark — letting us know what the market is thinking about the price of home finance. It is no more than an indicator of value. It’s not something that we buy or sell. It’s rather a benchmark.

It’s something like any other benchmark — whether the product being sold into that particular market is halal or not is a separate matter. The point is that the market looks at that product from a certain perspective, and that’s what interest-based benchmarks give us. It’s not that we participate in interest — it’s that we’re able to judge for ourselves what the market is doing.

The pricing of goods and services — whether cars, airplanes, boats, or clothing — is dictated by the market. Similarly, that’s what happens in the home-buying market.

DR. IMRAN USMANI

If I could add one very important principle of Shariah: the pricing of goods can be agreed upon by both parties at any price provided there is no misrepresentation. In Guidance Financial Group’s structure, the equity is not bought out at market price — they are going to sell the equity at par value. That is allowed because it is feasible for this market.

Now, when we come to charging a rental to use that particular portion — someone might say: you’re charging that particular amount, and the other person says, no, maybe the market is different. So we agreed: whatever the benchmark or scale of interest — which basically determines a rate of cost of funding — we will use that particular rate to rent out that particular thing on that basis.

The rental will not change daily. For today and the next 3 months, we fix a particular rent based on today’s benchmark. After 3 months, maybe 6 months, maybe 12 months, it will be reconsidered by both parties as the market changes. In leasing, it is allowed to change the rental after some period for future upcoming periods. This is allowed by Shariah.

Now why are they using the interest rate rather than any other rate? As per my father and as per the AAOIFI Shariah standards — this book also mentions that it is allowed to use that particular benchmark because it is just a scale for determining a particular cost of funding. And for example, just take an analogy: there is a particular market of shops, all rented out based on a certain rate related to a certain type of business. But one person wants to open a halal shop in that area. The landlord says: the whole market charges at that rate, so I will charge the same rental from you because it is the market price. That is allowed. Similarly, here they are charging a price based on the cost of funding and the natural laws of demand and supply of funding. If you go above or below that price, in either way the business is not feasible.

Considering all these aspects, scholars have allowed this and unanimously said it is just a mechanism to determine a particular rental price. But it is not uncertain — it will be fixed on day one for the upcoming 3 or 6 months, and then by mutual pre-agreed benchmark it will change for the next period.

If you want to learn more about that, all these things are described completely in the frequently asked questions on the Guidance Financial Group website, and in my father’s books and my own books.

HUSSAM QUTUB

These are really great answers. I recall nearly 20 years ago when I asked this question and heard from our founder and from Shaykh Yusuf: if we price our utilization fee too high, nobody will use us and we’ll go out of business. If we price it too low, we won’t have any investors to invest in these Musharakahs. So actually, being competitive — benchmarking to whatever that rate may be — is how we establish the utilization fee.

Now we’re facilitating that structure in a halal manner. Our contract is what makes something Riba-free. And frankly, if you look at our website, there’s a white paper that gives a very detailed explanation of the pricing model and how it works to establish the utilization fee.

One analogy I’ll end with — it’s a little funny, but it made me laugh: if you want to buy potato chips, potato chips are halal. There’s no madhab that says potato chips are haram. But here in the United States, if you go to a store, you should read the ingredients of how that potato chip was produced, because you’ll find that some are fried in lard — pig fat. Now something halal became haram. But if you wanted to sell halal potato chips, you would get the best potatoes and fry them in vegetable oil — and then sell them on the same shelf as the haram potato chips. How are you going to price it? You’re going to price it competitively with those fried in lard. If those are 99 cents a bag, you’re going to be 99 cents a bag. That doesn’t make it haram. What makes something Riba-free or Riba-producing is the contract. Our contract is what matters here.

LAILA KHAN

Thank you so much for that very thorough response. I did want to remind our attendees that we have that PDF available to download. Dr. Imran mashallah shared a number of different books — we will include those titles in our follow-up communication along with some other publications on Islamic finance that Shaykh Yusuf has contributed to as well.

We are at 2:30 now. We wanted to be respectful of everyone’s time, and mashaAllah we have hundreds of people still with us. We’re so grateful for your time on this Saturday afternoon. I want to give an opportunity for our dear esteemed scholars to share some final thoughts.

Shaykh Yusuf, would you like to share some final thoughts?

SHAYKH YUSUF TALAL DELORENZO

Thank you, everyone, for attending this afternoon or this morning. This has gone on a little bit longer than we’d anticipated, but that’s because of your interest — and we’re happy to accommodate that.

In short: alhamdulillah, Guidance Residential has established itself as the largest, the oldest, and the most successful of all Islamic home finance companies here in the United States. It has done so equitably, with great transparency. They’ve provided consumers like you and me with enormous amounts of information, especially on their websites — white papers, FAQs, and so on. But they’ve also sponsored talks like this constantly over the years and sponsored special visits to communities around the country. Mashallah, they’ve done a wonderful job, and we can only wish them more success in the future, InshaAllah.

DR. IMRAN USMANI

I add to what Shaykh Yusuf Talal DeLorenzo said. It is really a very great success story in a country like the U.S., which has so many states and different regulatory issues. To comply with all those regulatory issues while also maintaining Shariah compliance was really challenging. But alhamdulillah, they structured it to comply with both Shariah and regulation. It was very challenging, but mashallah they accomplished that particular task.

Alhamdulillah, it is a blessing from Allah subhanahu wa ta’ala. And blessing comes from the acceptance of the people. Alhamdulillah, people have accepted this particular program. For the last 25 years, we have seen in so many gatherings like this — enormous interest from the audience and always so many questions. To question is half of the knowledge. Asking questions to explore knowledge is very important for increasing our knowledge, and it is very much appreciable.

I appreciate all — the management of Guidance Group as well as all the audience who participated with such great interest in this subject. Alhamdulillah. May Allah give them very good rewards, make the whole program more successful, and make it acceptable in Allah’s eyes. Subhan Allah. Please forgive me if I said something that may not have been understood due to my language barrier. I hope you have understood my points clearly, InshaAllah.

SALMAN ALI

JazakAllah khair, Dr. Imran, Shaykh Yusuf, Laila, Hussam, and everyone who’s still with us for your time. And I want you to know that this is just the start. This is not the end. It’s the end of our session, but it’s the beginning of starting your journey of halal home ownership.

A lot of folks ask: what’s the first step? The first step is to scan the QR code, get online, submit your online pre-qualification and pre-approval. InshaAllah you’ll be connected on Monday with a licensed, knowledgeable, professional account executive local to your area, and we’ll guide you through the next steps. Many of you had many questions and I promise you, InshaAllah, all of your questions will be answered. Thank you again to everyone here.

HUSSAM QUTUB

First I want to thank Dr. Imran Usmani and Shaykh Yusuf Talal DeLorenzo. It’s an incredible privilege to have both of you here with us. We couldn’t have asked for more. We’re incredibly fortunate to have not just you, but the other members of our Shariah supervisory board along this journey. Our regards to them as well for everything they do and have done to get us to this level.

To the audience: thank you for joining us and spending your Saturday — two and a half hours with us. We hope you learned a lot from this session. As Salman said, this is not the end. This should be the beginning of your journey. You attended for honorable reasons: to ensure that your journey on home ownership is rewarded by Allah. There’s baraka under the roof that you live in. We want to reassure all of you that as we’ve helped nearly 45,000 households across this country achieve the dream of home ownership in a Shariah-compliant, blessed manner, we aim to serve you as well. We look forward to working closely with you and establishing generational wealth for you and your family in the most Shariah-compliant manner possible. Please scan that QR code and let’s begin the conversations.

LAILA KHAN

Thank you to each and every one of you for giving us your time. Again, it’s a great privilege and honor to sit with Shaykh Yusuf and Dr. Imran to go over this very important subject matter — Islamic finance. It touches all of our lives, and InshaAllah we are so grateful to be a part of your next steps toward a halal lifestyle. This is just the beginning. You’re going to see follow-ups from us with the resources we shared. Have a wonderful weekend and rest of this year. We look forward to more engagement.

Key Takeaways

Guidance Residential is not a bank. It is Muslim-owned and Muslim-led, with no ties to a conventional Riba-based bank or lender, so profits never flow back into interest-based banking.

This is co-ownership, not a loan. Guidance and the homebuyer purchase the home together through a declining balance partnership (diminishing Musharakah), and the homebuyer’s ownership share grows with every payment.

Guidance shares real risk with customers. Financing is non-recourse, late fees only cover actual administrative costs (never profit), and losses from events like natural disasters or eminent domain are split based on each partner’s ownership share at the time.

Homebuyers keep 100% of the appreciation. Because customers use the entire home and are responsible for its maintenance and property taxes, they also receive the full benefit when the home’s value goes up.

The profit rate is benchmarked to market rates for comparison, not because the contract works like a loan. Shariah permits using a market rate as a benchmark for a fair rental price. What makes financing halal is the underlying contract, not whether a number resembles an interest rate.

An independent Shariah Supervisory Board oversees the program, including annual audits, to confirm the structure stays fully compliant over time.

Guidance Residential has provided more than $10 billion in financing to more than 40,000 families over 25 years, with programs now available in 35+ states.